FEATURES: The advisors at Letterkenny Credit Union take a look at the alternative ways to purchase a car, examining the rising trend of personal contract plans and weighing them up against typical car loans.

There’s a lot to be said for simplicity. For having a full understanding of the situation at hand. For not being confused or worrying about the small print or the hidden details.

Take buying a car. It used to be easy. You decide which car you want to buy, you find out the cost of buying it, perhaps the trade in value for your own car and then work out if or how much you need to borrow to pay for it. Simple.

For anyone who has tried to finance a car purchase in recent times, the process can be far removed from this.

One emerging trend in car finance is the introduction of Personal Contract Plans (PCPs). Essentially a PCP is a lease scheme which makes financing a new car seem affordable for lots of us with low monthly repayments.

Here’s how it works:

Typically, a person will be offered a PCP package at the forecourt when buying a car. The buyer will be asked to pay an initial deposit (usually between 10% and 30%) and then agree a monthly repayment – usually over the next three years. PCPs generally have low monthly repayments, which can make them seem more affordable when compared to other forms of finance.

The provider guarantees a minimum future value (MGFV) for the car taking into account depreciation and wear and tear.

The MGFV is the amount you will have to pay to own the car at the end of the agreement. It is calculated by the finance company, based on its estimate of the future value of the car at the end of the agreement. It takes into account such things as, the car you are buying, length of agreement, the condition of the car at the end of the agreement and your annual mileage.

At the end of the term of the PCP, the buyer is left with 3 options….

– Pay a final payment (the minimum guaranteed future value or balloon payment) and keep the car.

– Hand the car back. Be aware that if you do opt to hand the car back, you don’t get anything from the car dealer for its value no matter how well you have kept it and maintained it and you might end up having to pay if you have not complied with all the terms and conditions.

– Put the car down as the deposit on another car and enter into a further PCP. It is important to be aware that the deposit you put down for the first car will not be available when you give the car back to use when taking out a new PCP. The equity you have built up in your monthly repayments and the difference of the MGFV is what you would have to put towards the new car. All you have to put towards the new deposit is whatever equity you built up from the first PCP. This equity may be less than the deposit required for rolling it over so you will need to top the deposit up each time.

With a PCP agreement, you don’t own the car, you are hiring it for a period of time, typically 3-5 years. You only own it when you make the final payment. This is important because if you were to run into financial difficulty during your PCP agreement, unlike a personal loan, you cannot sell the car to pay off your debt.

These agreements are among the least flexible forms of finance. Because the payments are fixed for the term of the agreement, you cannot usually increase your repayments each month if you wish to do so. If you want to extend the term, you may be charged a rescheduling fee.

Before agreeing to a PCP make sure you always read the small print before you sign up. For instance, the cap on the number of miles/kilometres you are allowed to clock up over the period of the agreement. They may also request that you commit to certain car servicing requirements.

Always enquire about any additional fees and charges. You are entitled to a list of all additional charges and fees, so ask the garage for this before you sign up to any agreement.

For instance, ask if there is any documentation fee for setting up the agreement, missed repayments fees or repossession charges.

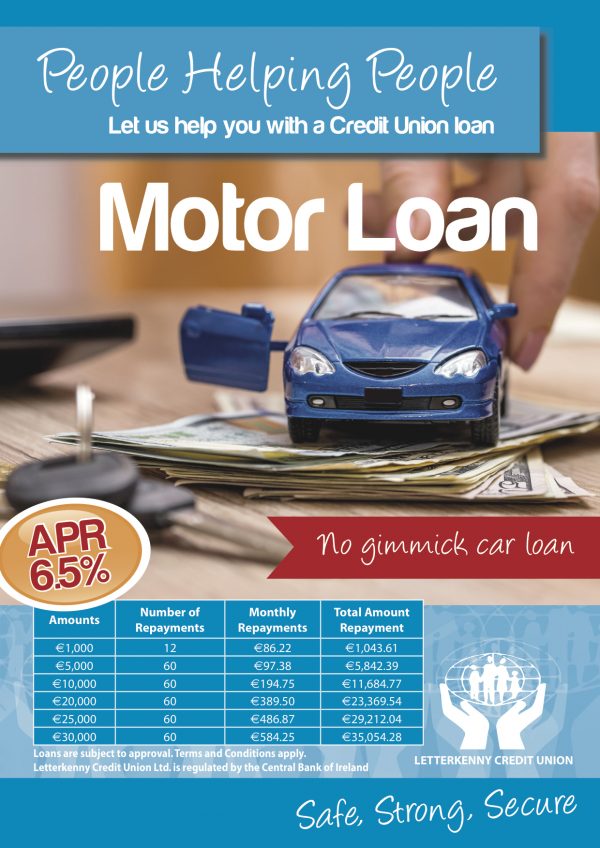

Letterkenny Credit Union Car Loans

∙ Unlike a PCP you own the car from the outset

∙ You can sell the car on at any time

∙ You can borrow for the full amount

∙ There are no hidden fees, admin charges, transaction charges, set up costs or balloon payments

∙ The interest you pay on a credit union loan is the full cost of the loan so it is fully transparent

∙ Letterkenny Credit union interest rates are fair and reasonable and capped by law

∙ Repayments are calculated on your reducing balance, so you pay less interest with each repayment

∙ Your credit union loan is insured in the event of your death – subject to terms, conditions and eligibility criteria – at no direct cost to you

∙ You can pay off your loan early, make additional lump sum repayments or increase your regular repayments, without a penalty. Other lenders may charge you extra for paying them back faster!

When comparing finance options, take the time to compare the total amount payable on a credit union car loan (cost of credit) with the PCP cost (the deposit, plus monthly repayments and final payment). Make sure you also compare the terms and conditions of each option.

An issue with a PCP is that it can restrict what you do with the car during the term. If you’ve taken out a credit union loan, then the car is yours to do with as you please. Drive as many miles as you please and crucially, sell it if you need to.

The way a PCP is structured can set up a situation where the easiest and simplest option is to roll over into a new car and a new plan.

PCP’s are, in effect, a way of trying to ensure that you will come back and buy another car from the same dealer or manufacturer.

All well and good, but what if you don’t like the brand of car or range they have to offer anymore? It does seem a little like saving money in the short term by spending more over a longer period. Our advice – read all the small print and be fully aware before you sign on the dotted line.

If you’re thinking about your options for financing a car purchase, look no further than Letterkenny Credit Union.

For further information please contact Letterkenny Credit Union on 0749124166.